I was tasked by IDEATE to do research Digital Banking early on and after completing multiple Fintech projects, I was assigned to do a broader research specifically on Neobanks and understand it from a user experience perspective.

Journey

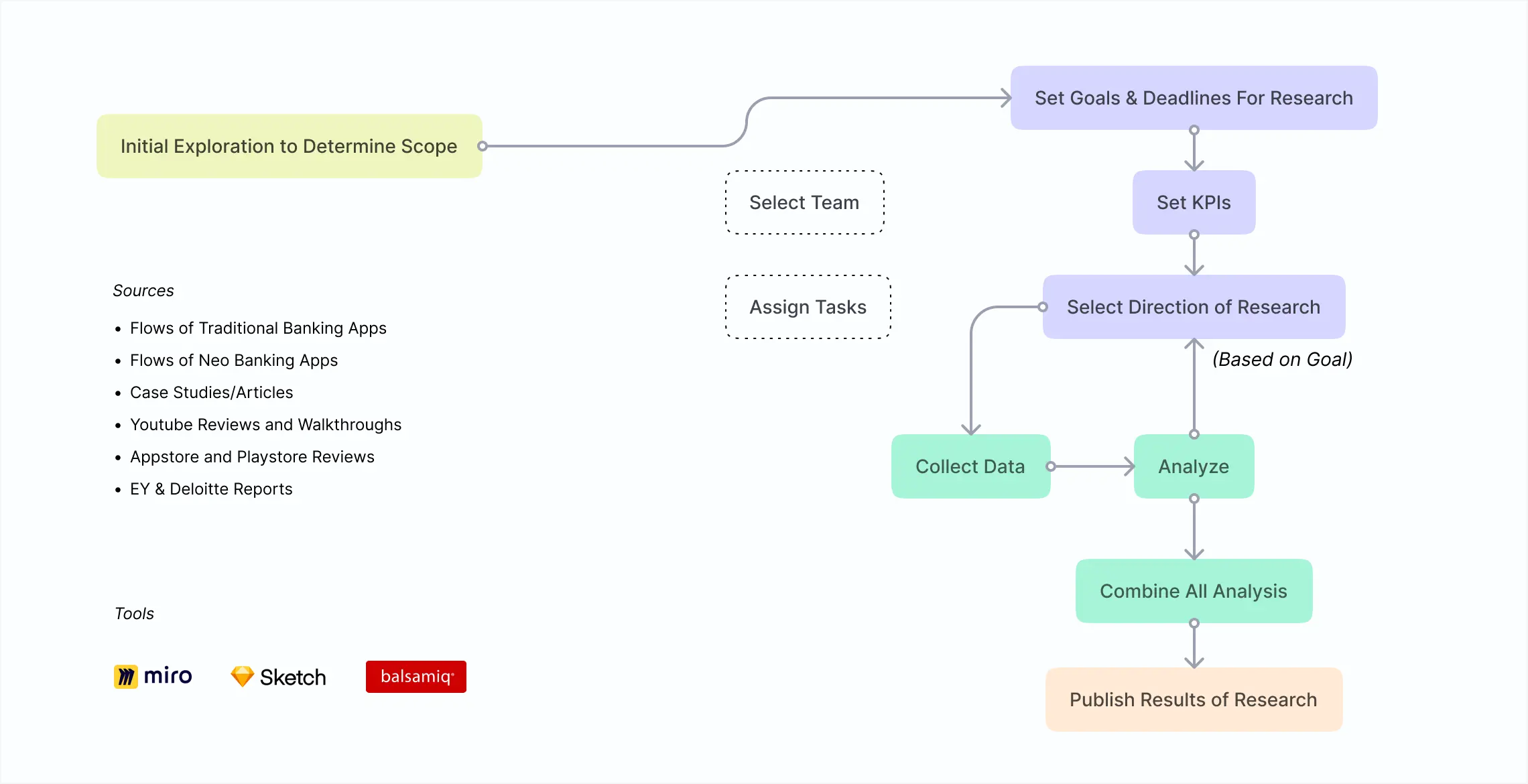

It started in the early 2019 after we got KFH as a client, the CIO Umair asked me to spend sometime researching on digital banking and look at the role of UX and CX in it.

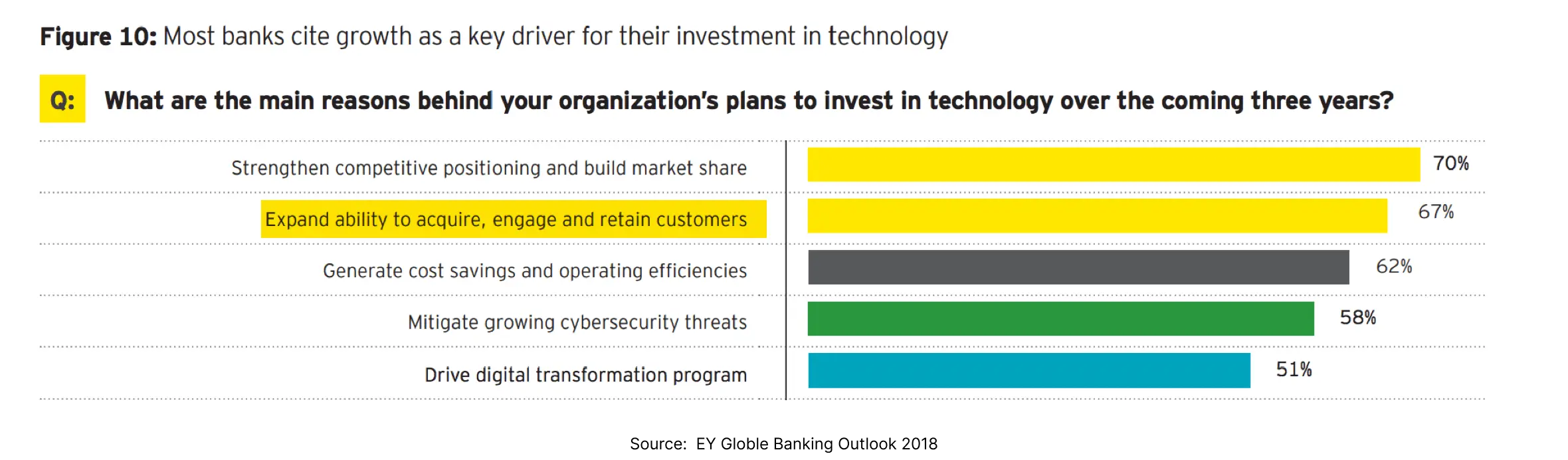

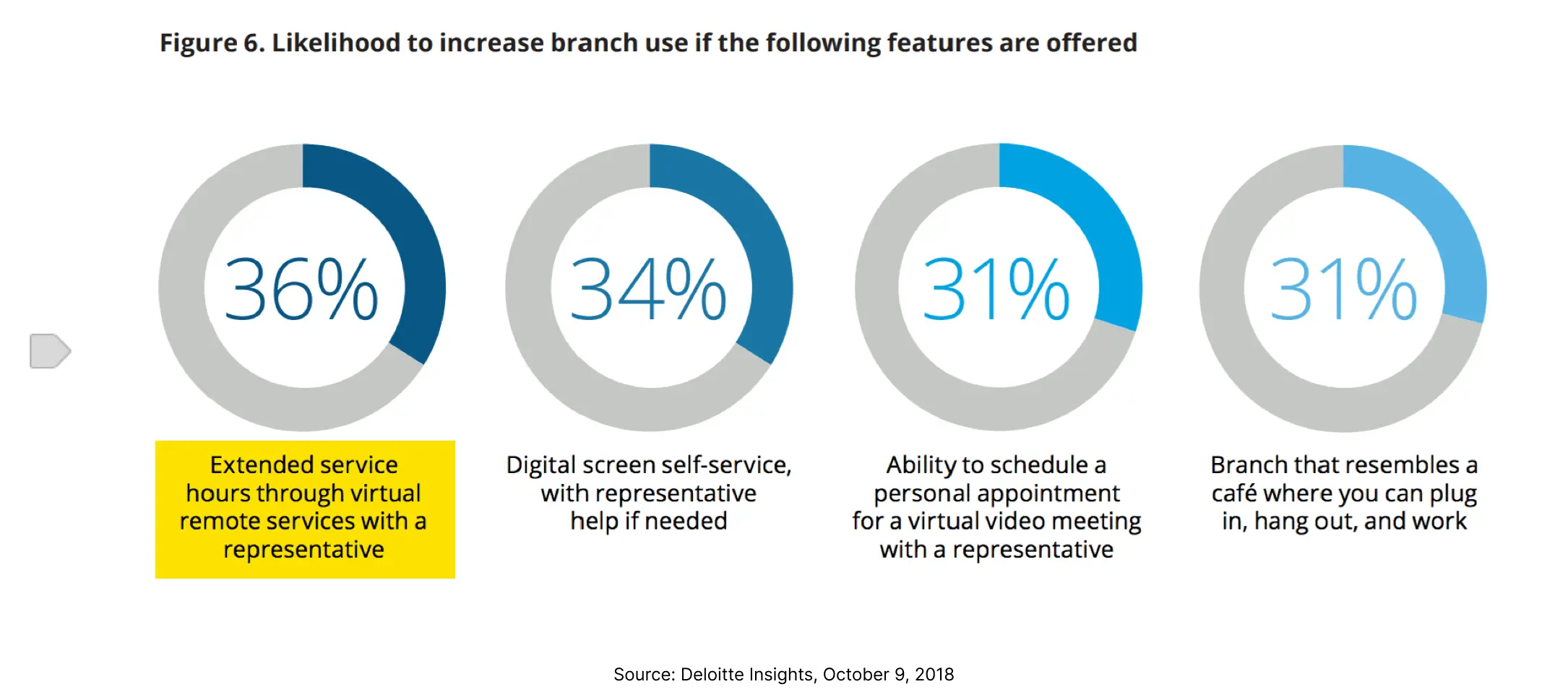

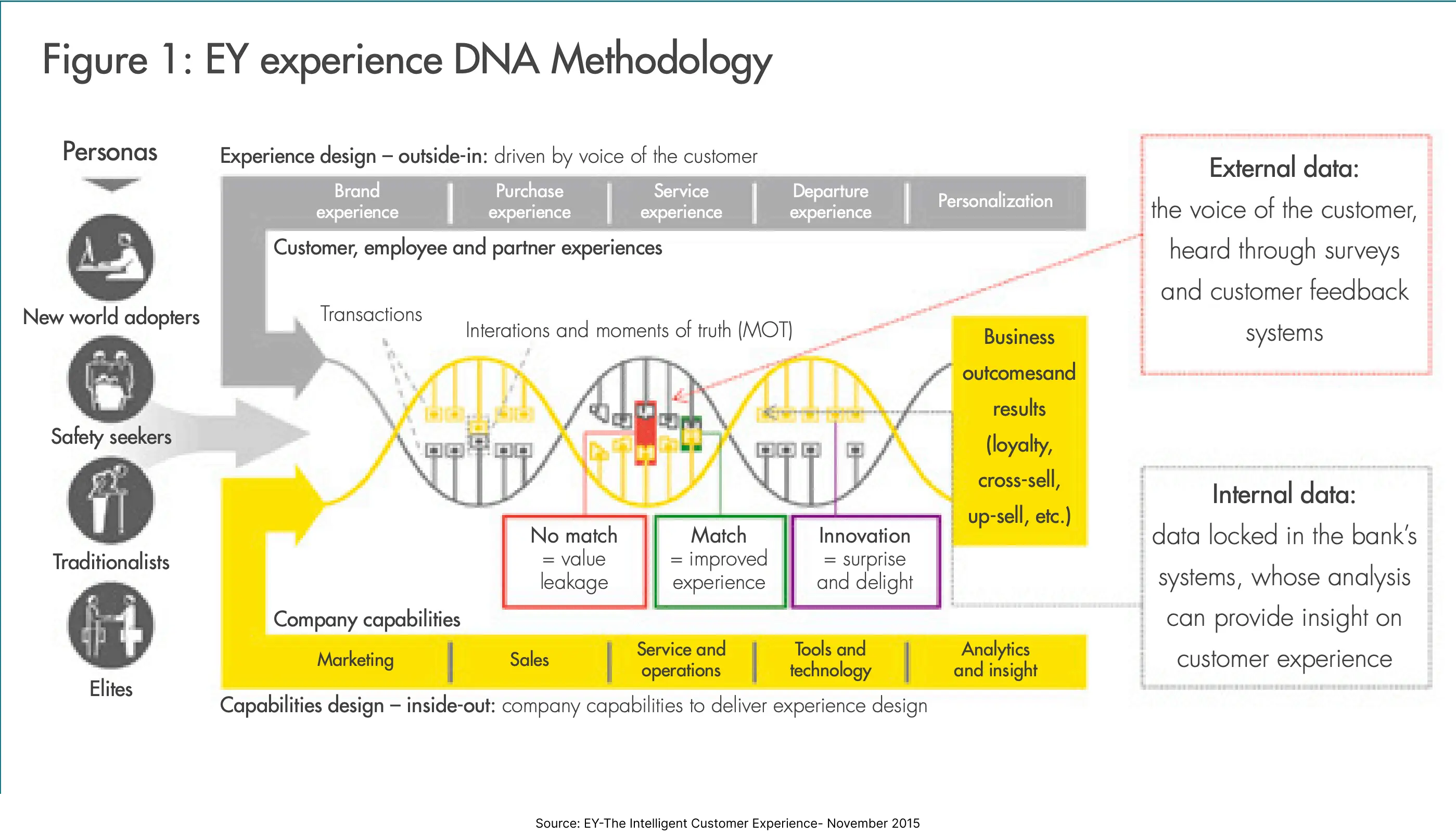

The data that I came acorss was crystal clear, CX and UX were shown as a priority for banks and rightly so. With the extended ability to develop and introduce features in the market, experience becomes one of the keys to successfully retaining customers.

Bonus: CX Touchpoints by EY

A Fascinating Tangent

Along with learning how key experiences have become to this game, their was another dimension of this which I found interesting.

Prior to this research, my intuition was that traditional banks as being opposed to digital transformation and only doing it due to force from the outside. While this was somewhat true that banks wanted to maintain legacy systems, the reaons of this behavior were far complex than “the old generation doesn’t want to change”.

Even if the banks wanted to change, the inherent disconnect between the spirit of innovation of technology and the rigid processess required for strict security doesn't make things easy. Furthermore, the pace of innovation and security isn’t compatible. Technology evolves at a much higher pace than many other fields. Imagine spending a year and a few millions on updating to a new technology only to know that a newer one is now the standard. New technologies might be prone to unforseen failures which you might not be able to afford.

Another piece of the puzzle is figuring out how to keep the top “tech” people around in the cubicles. I don’t just mean the physical spaces even though they mean a lot for such talent.

Innovation requires out of the box thinking and new perspectives but merging them with the stricter security concerns and conservative view points of the managers is not an easy challenge. Add in tons of beaurocracy to the soup and you have got an environment that's a perfect repellent for the innovation.

The new comers exploited this to the max. Financial sector was long due for an overhaul and finally the stacked cards fell.

Financial Techonology

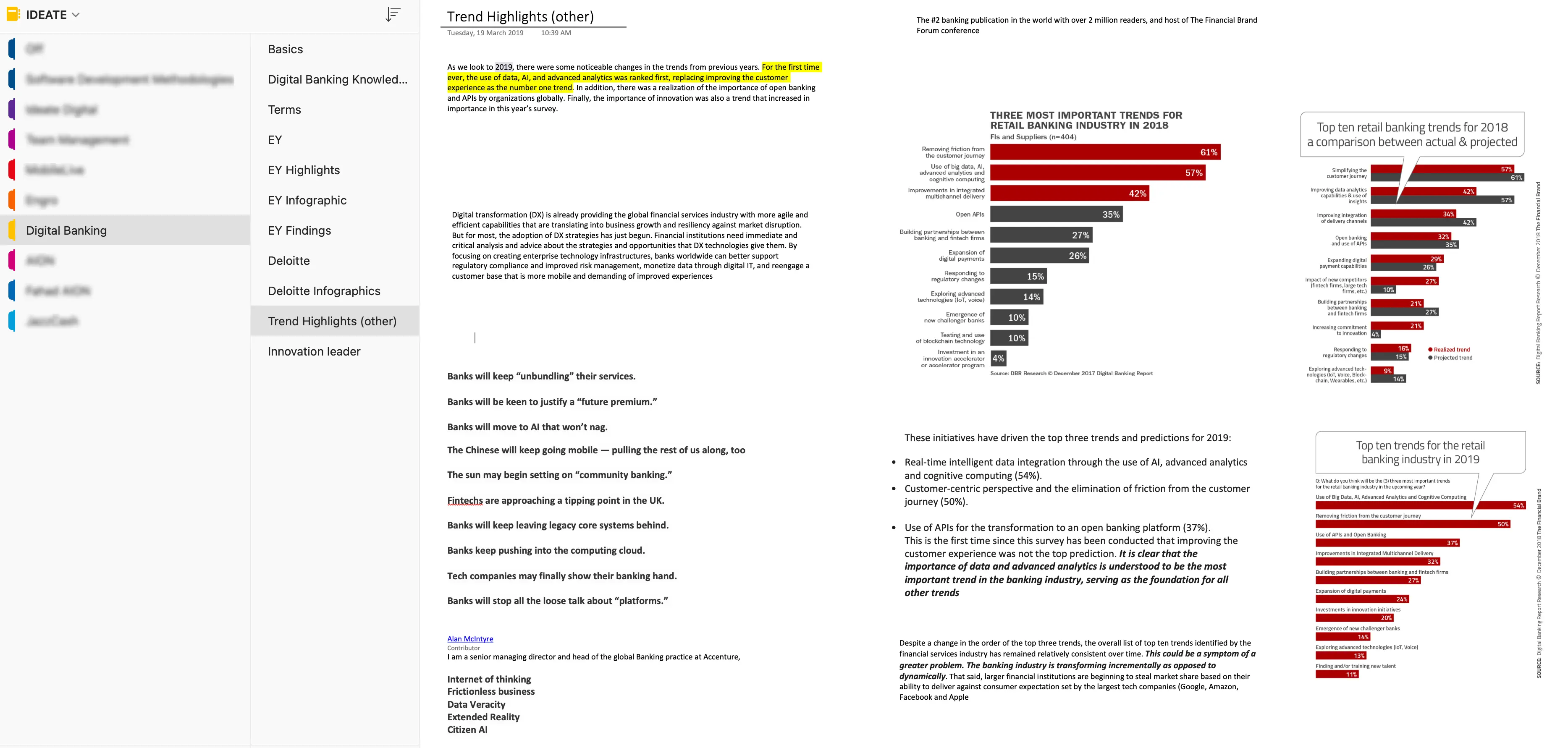

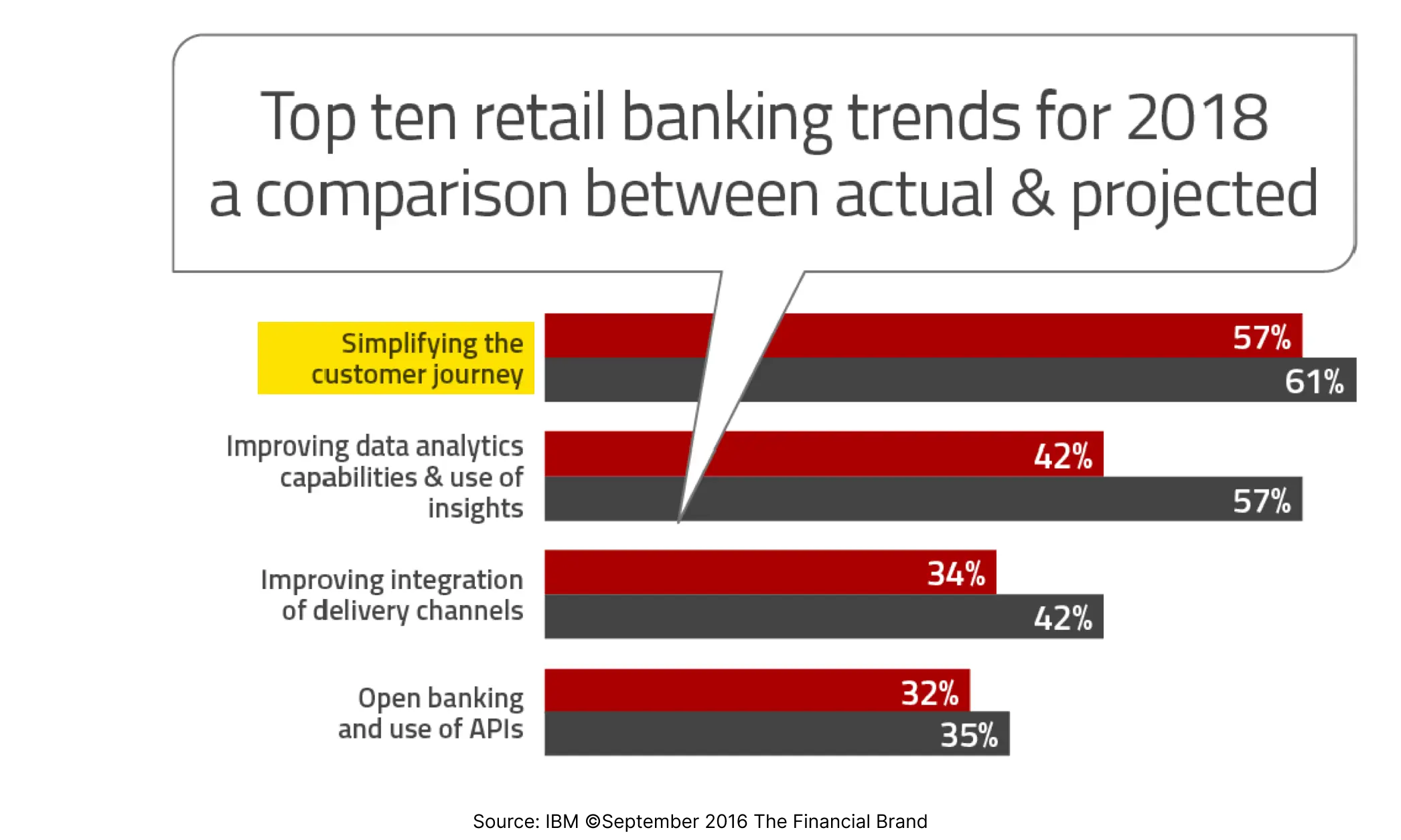

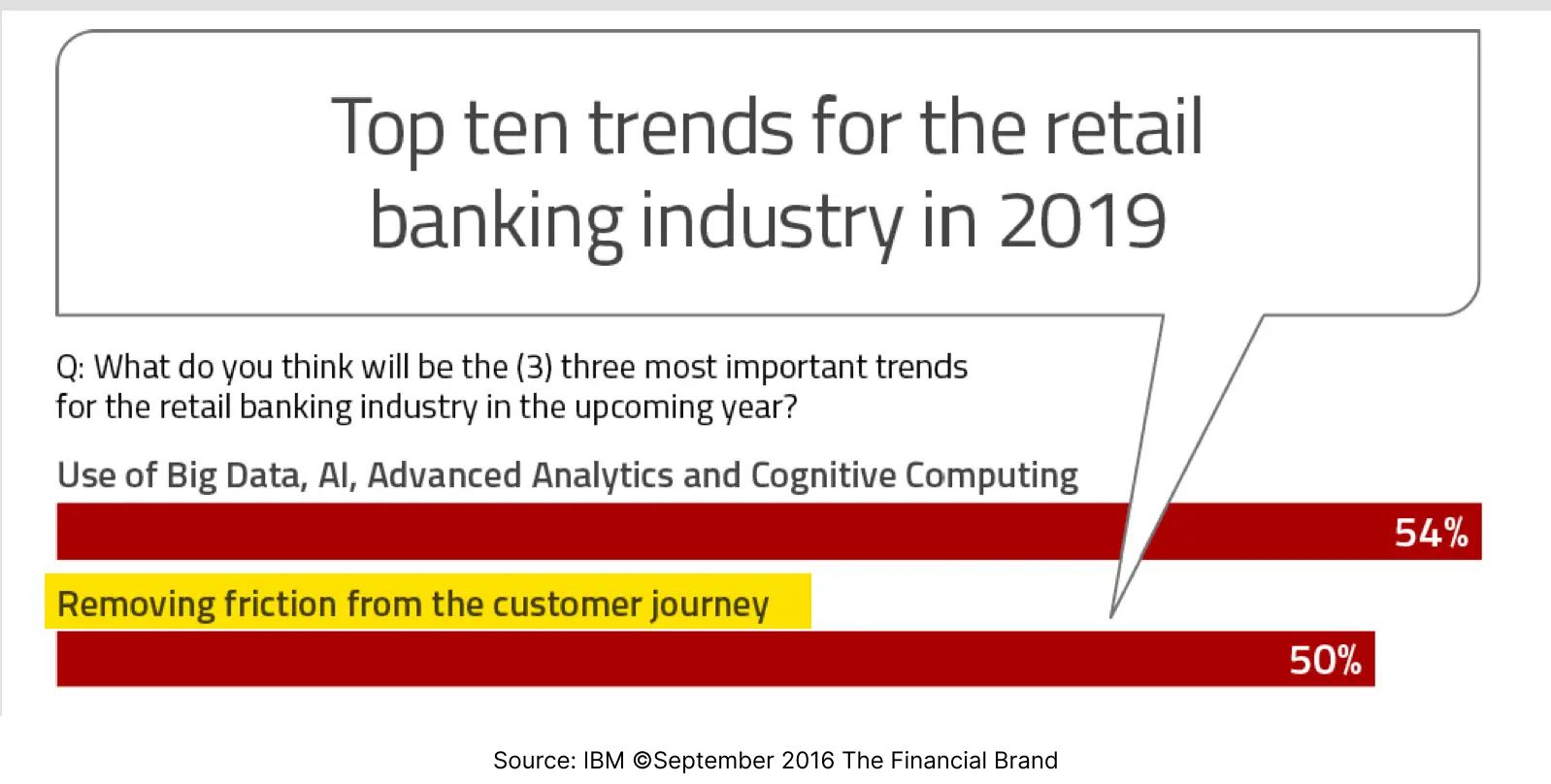

In 2017 the investment in Fintech was around $50 billion and as of January 2021, its ~$235 billion. The transaction have doubled from $3.04 trillion to $6.68 trillion in the same time period.

They won the war against banks but the only loser was old perspectives. Banks quickly joined hands with Fintechs with many investing in them.

Now this doesn’t mean the battle is finished. Traditional banking still remains a significant sector and while Fintechs can offer superior features, banks still have the advantages of being more experienced and the ability to navigate significant regulations. But this sort of survival doesn’t have to be negative for the customers.

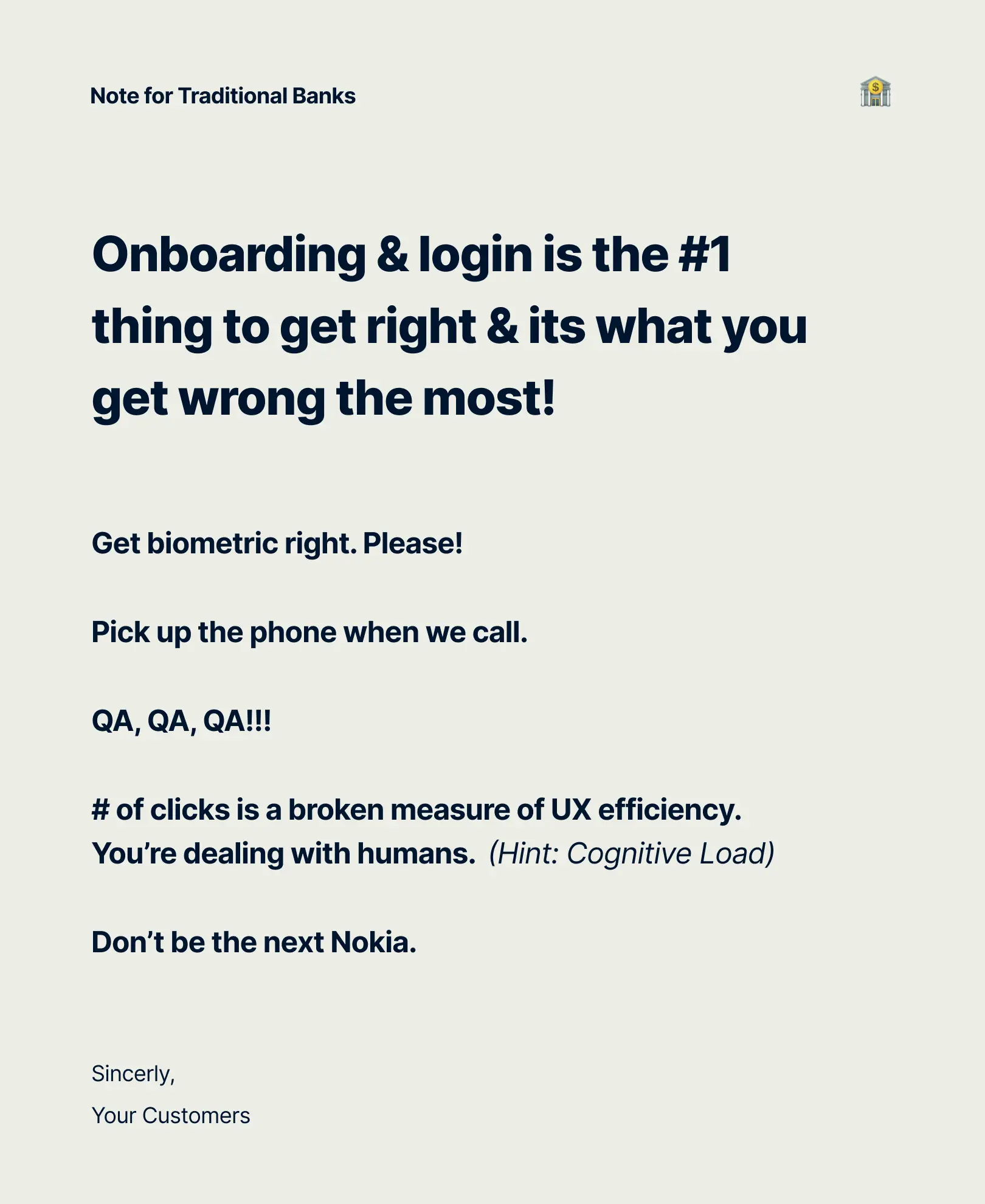

How to not suck as a traditional banking app!

The next step which I focused on in the second research was the UX of tradition banking sector apps. In many ways this was a natural yet unexpected evolution of previous research on digital banking. When you research on Fintechs, the whole idea is being able to do things digitally. Given that smartphones are the most used digital device in the world, apps were going to be the target sooner or later. But we followed a different route.

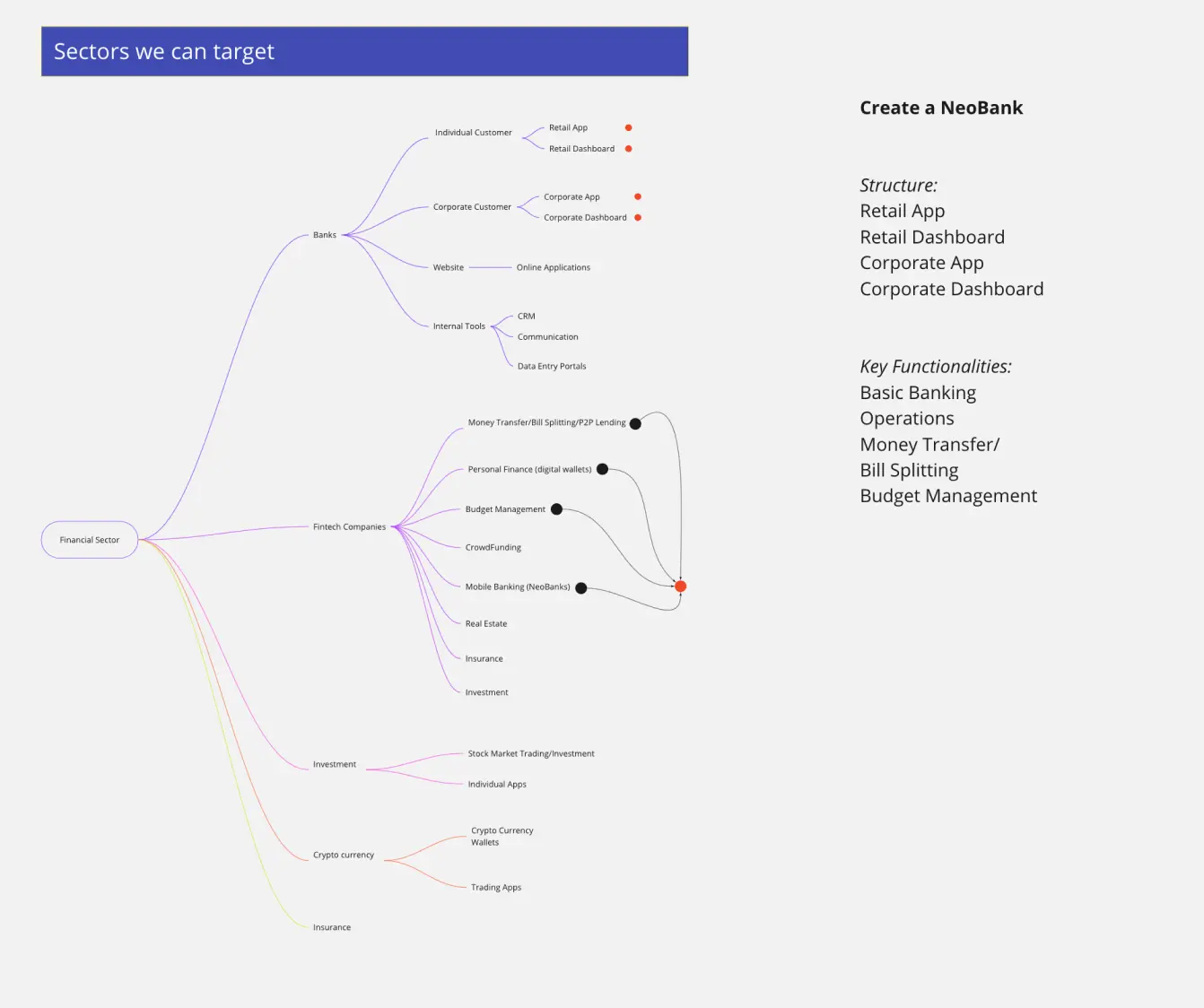

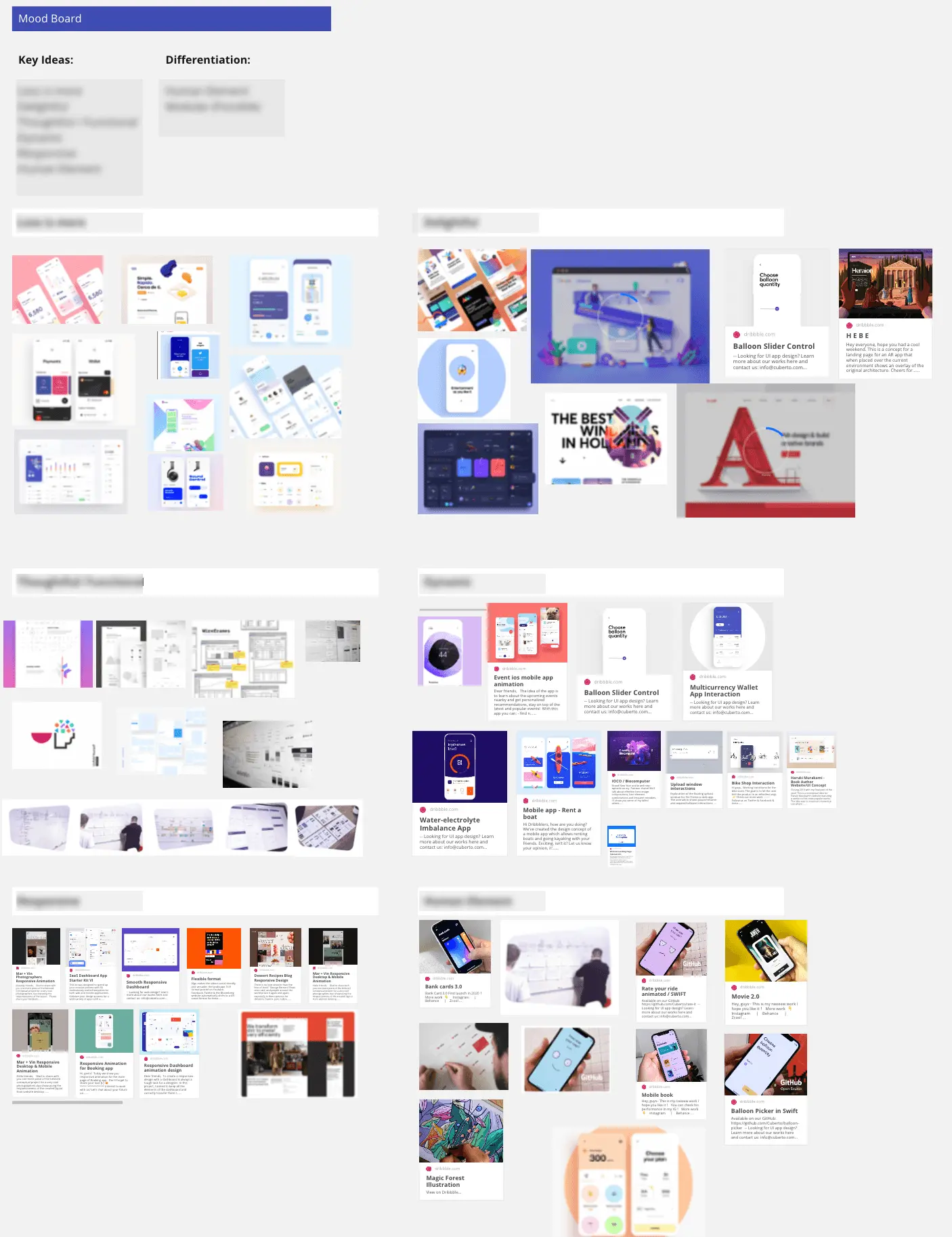

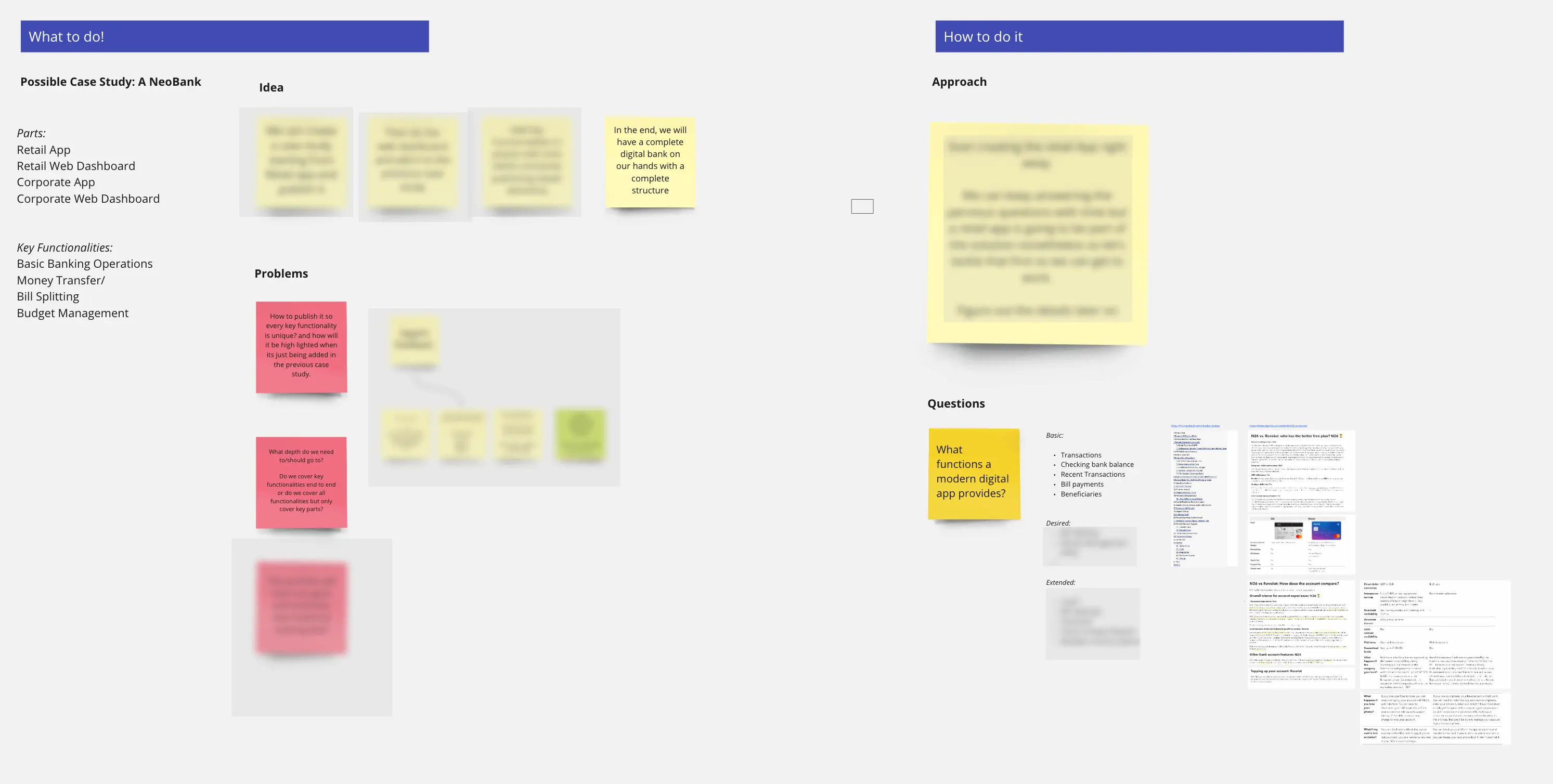

In order to learn about the fintech world, we decided to learn by experimenting. The idea was to design an experience of a Neobank. Along with this, I pitched the key ideas and then a mood board to respresnt what that could look like to my manager Umair. It was during the research of this neobank creation that we stumbled on to the contrast of experiences between neobanks and traditional ones. Parts of research have been redacted since they are protected and confidential as of now.

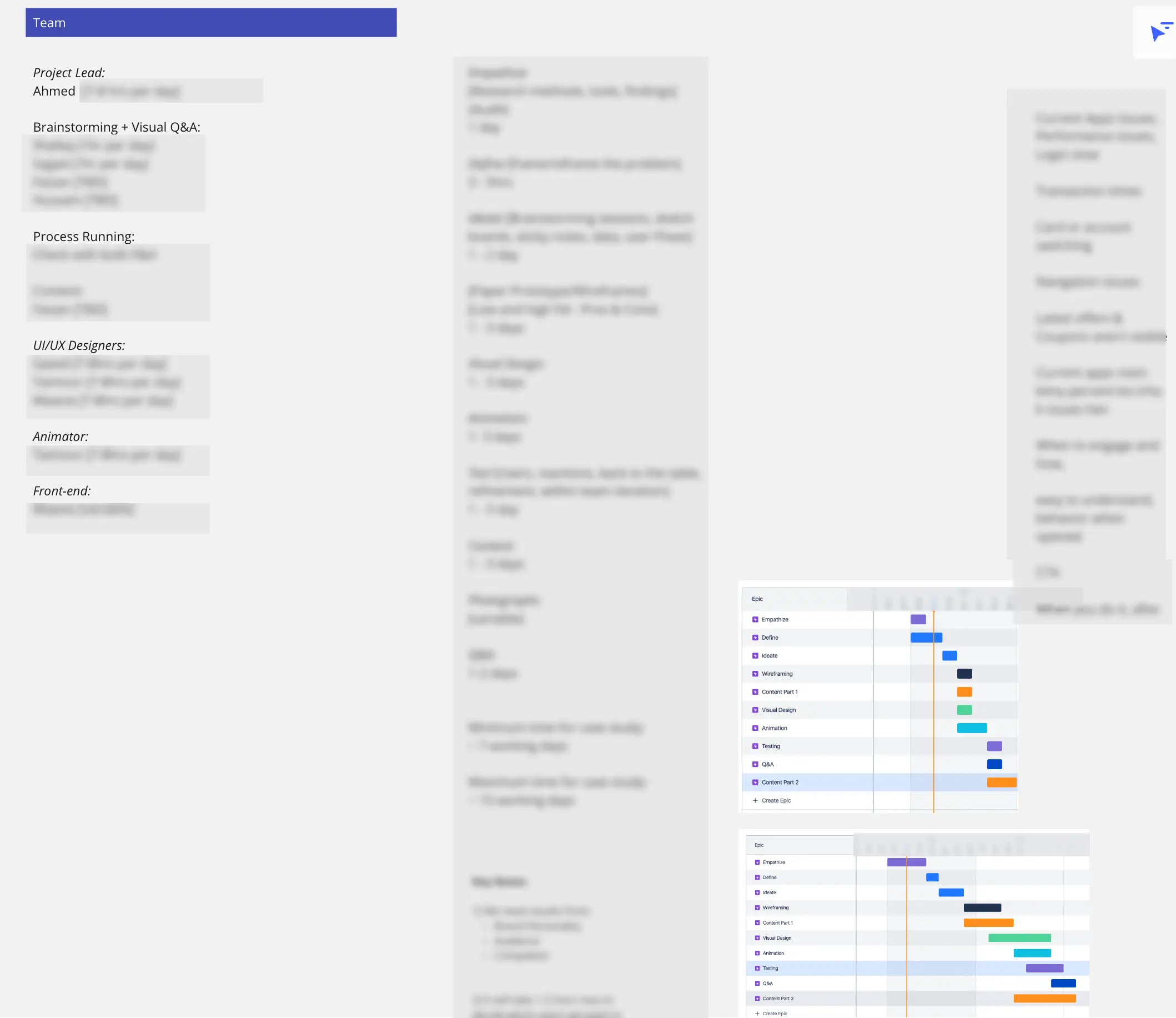

After getting that approved, I formulated the team and assigned tasks as per their experience. This involved creating a timeline which suits the delivery plans of our case studies based on the findings of our research.

Why fintechs apps are so loved?

One of the reasons should be pretty obvious

Our little consumer feedback hack completely backed this up. I turned to the easiest data I could find in order to find what’s going on i.e Reviews!

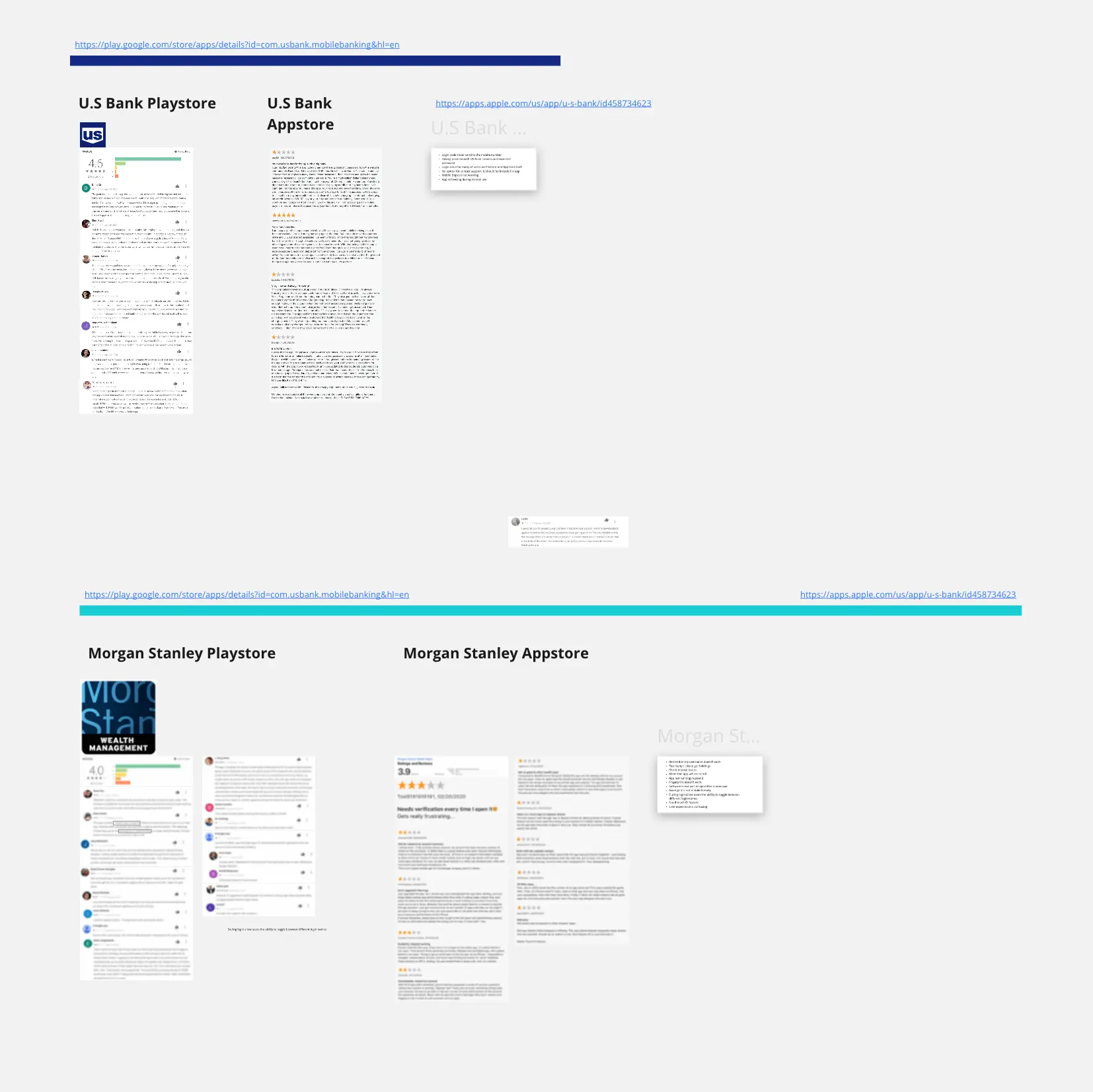

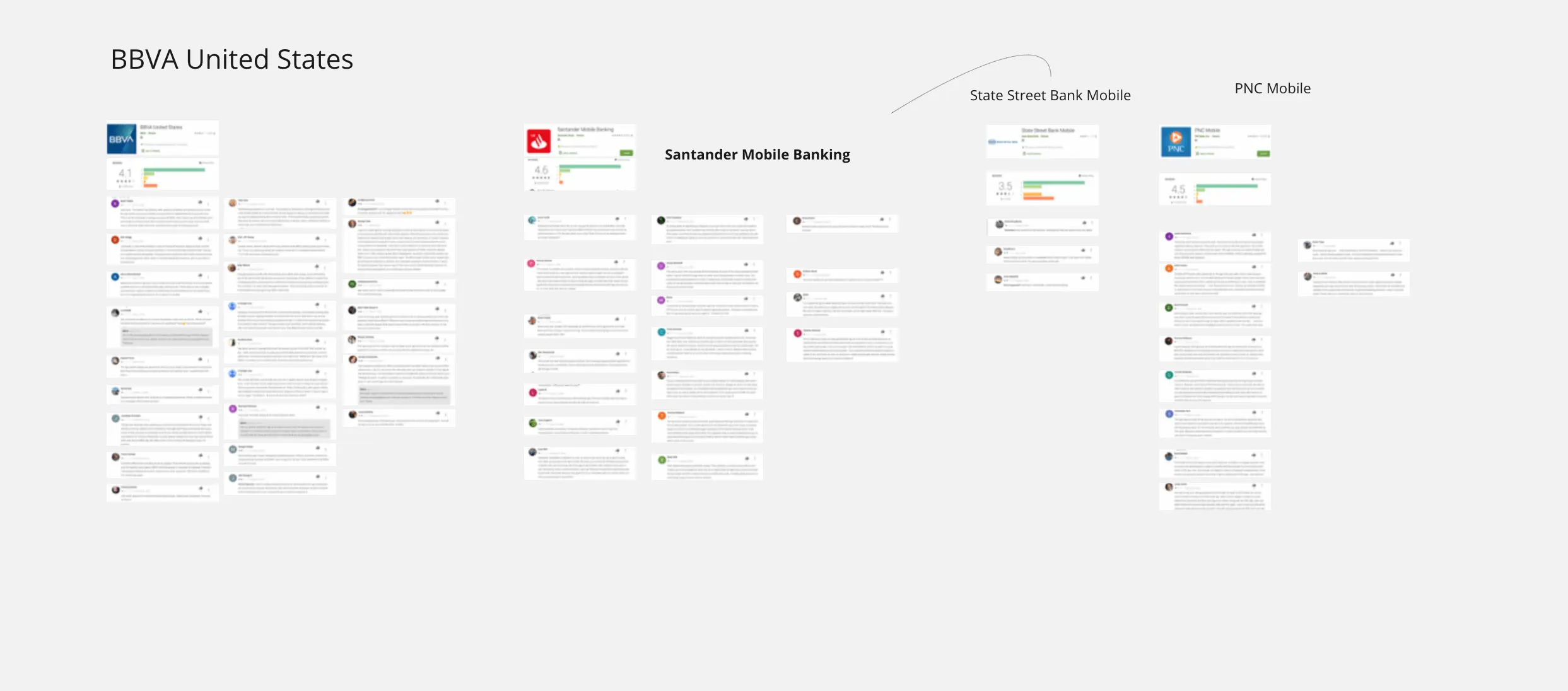

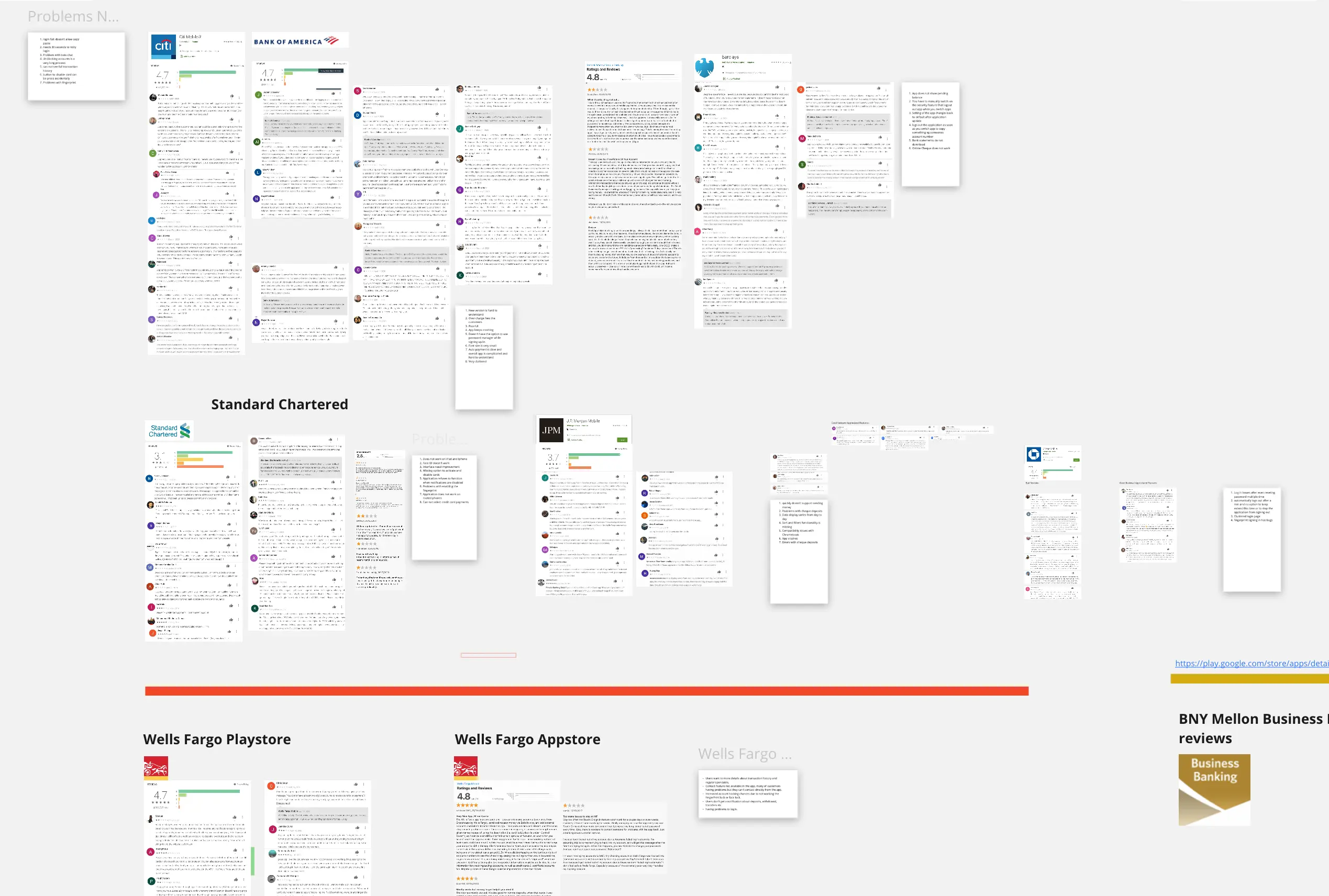

We spent quite a lot of time gathering Playstore and Appstore reviews of traditional banks. Following were the banks under consideration

What did they say?

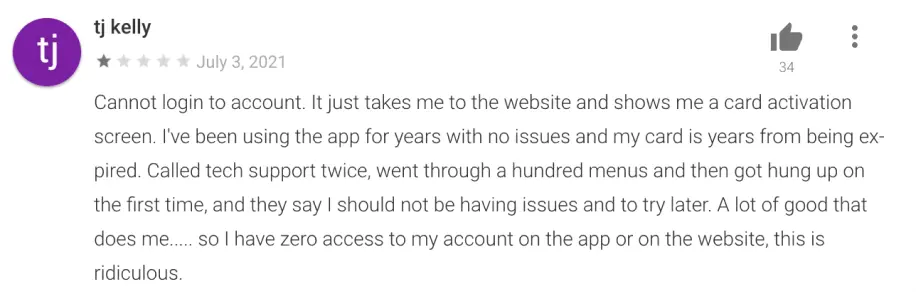

Nothing good. Its important to mention here that actual user reviews seem to tell a different story than ratings. Citibank has a rating of 4.7 but when you open the reviews, you find negative reviews being liked. While writing this case study, I took a look at top review on presented by default on July 8th 2021.

This review from Tj Kelly has accumulated 34 likes within 5 days of posting. Keep in mind that this is not happening on a social platform. Its burried in playstore feedback section.

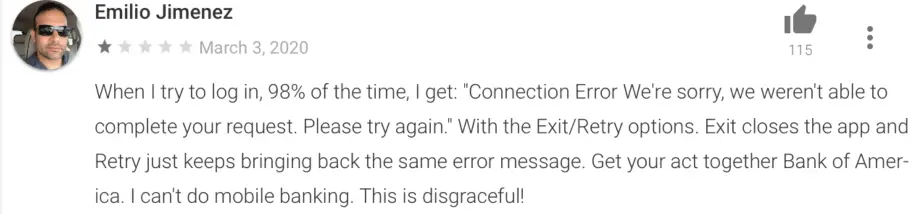

and its not unusual to find. This comment by Emilio Jimienez is a year ago for Bank of America and has 115 likes. To reiterate, this is not social media and gathering even 2 likes on a review is a big deal on such platforms.

Below are some screenshots of the reviews related work. We also collected notes about which issues were common with a specific bank so we can provide bank specific suggestions later on.

Surprise Surprise

Anyone who has used any app of any of the top Fintech will testify that the experience of traditional apps is worse but that’s not the surprising part. The surprise is at they all suck in the things which are pretty much key to the entire experience and they all have it common. As you might have noticed, both the above two reviews were mentioning login problems. Imagine the amount of frustration and loss of trust if the user cannot access his own money when needed.

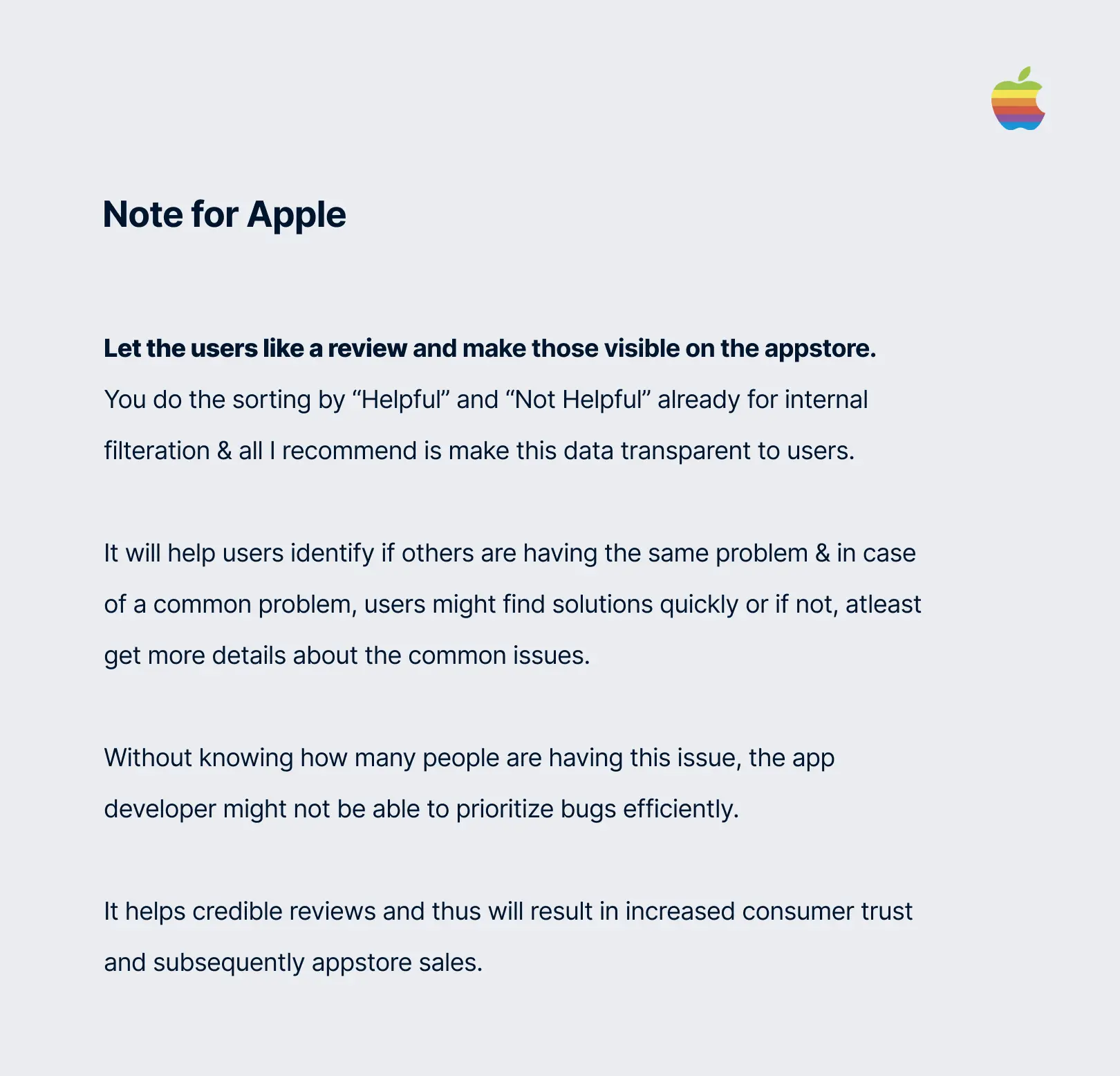

This study gave us 5 aspects on which traditional banks can improve and get guaranteed satisfactory results cause these were the the common problems among all apps so focusing on improving this already gives you an edge. These points will be published in the case study when that goes live.

How others won?

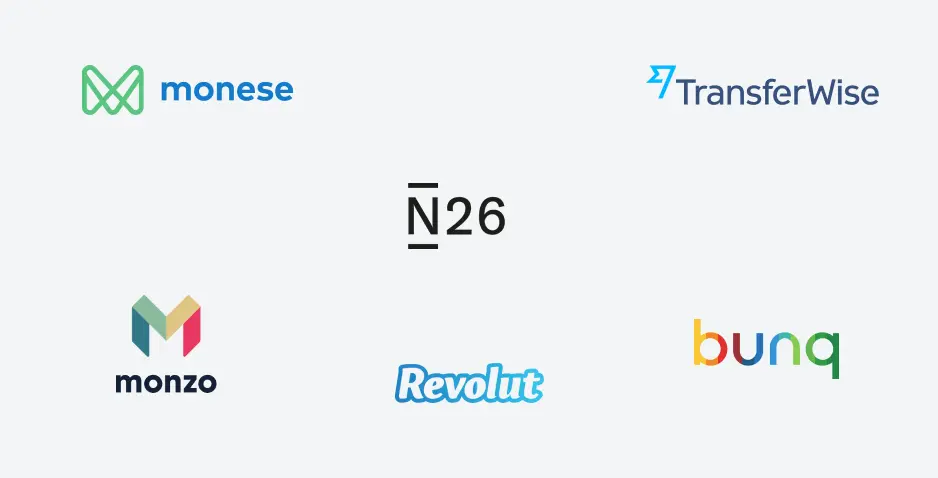

After understanding the common problems traditional apps have, we decided to learn from the winners. In total we studied 6 Neobanks.

Userflows

We couldn’t get access to every account in every bank but we devised a hack for that as well. We followed onboarding steps and experiences from youtube reviews and walkthroughs. Also classified their brands, mapped their journeys and the differentiating points.

Our prior experience in designing flows for Fintechs became super relevant here as well as we immediately connected with the intentions behind design decisions.

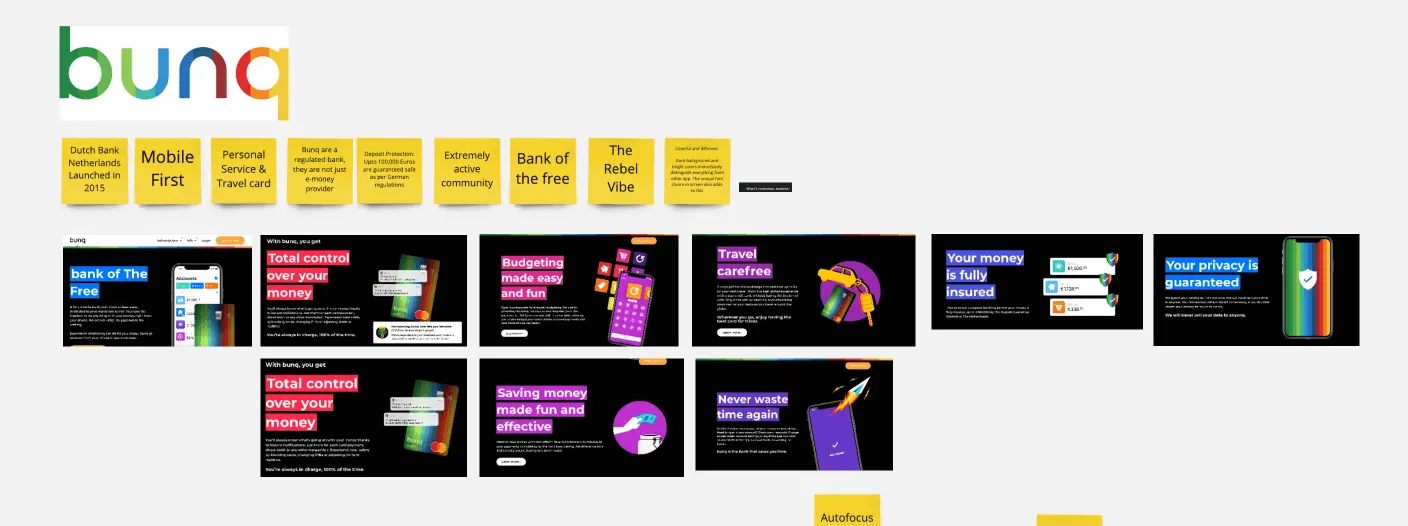

Onboarding

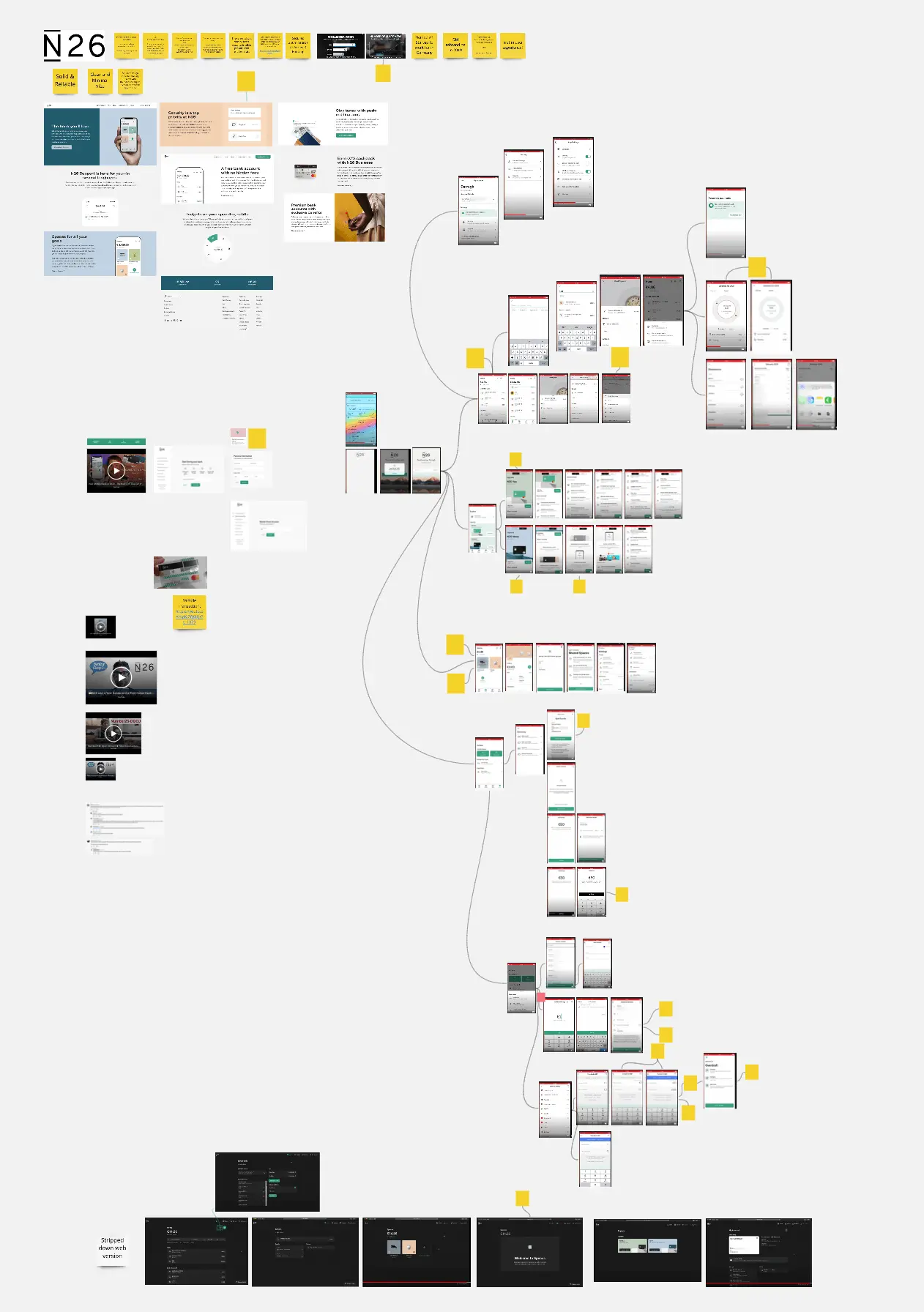

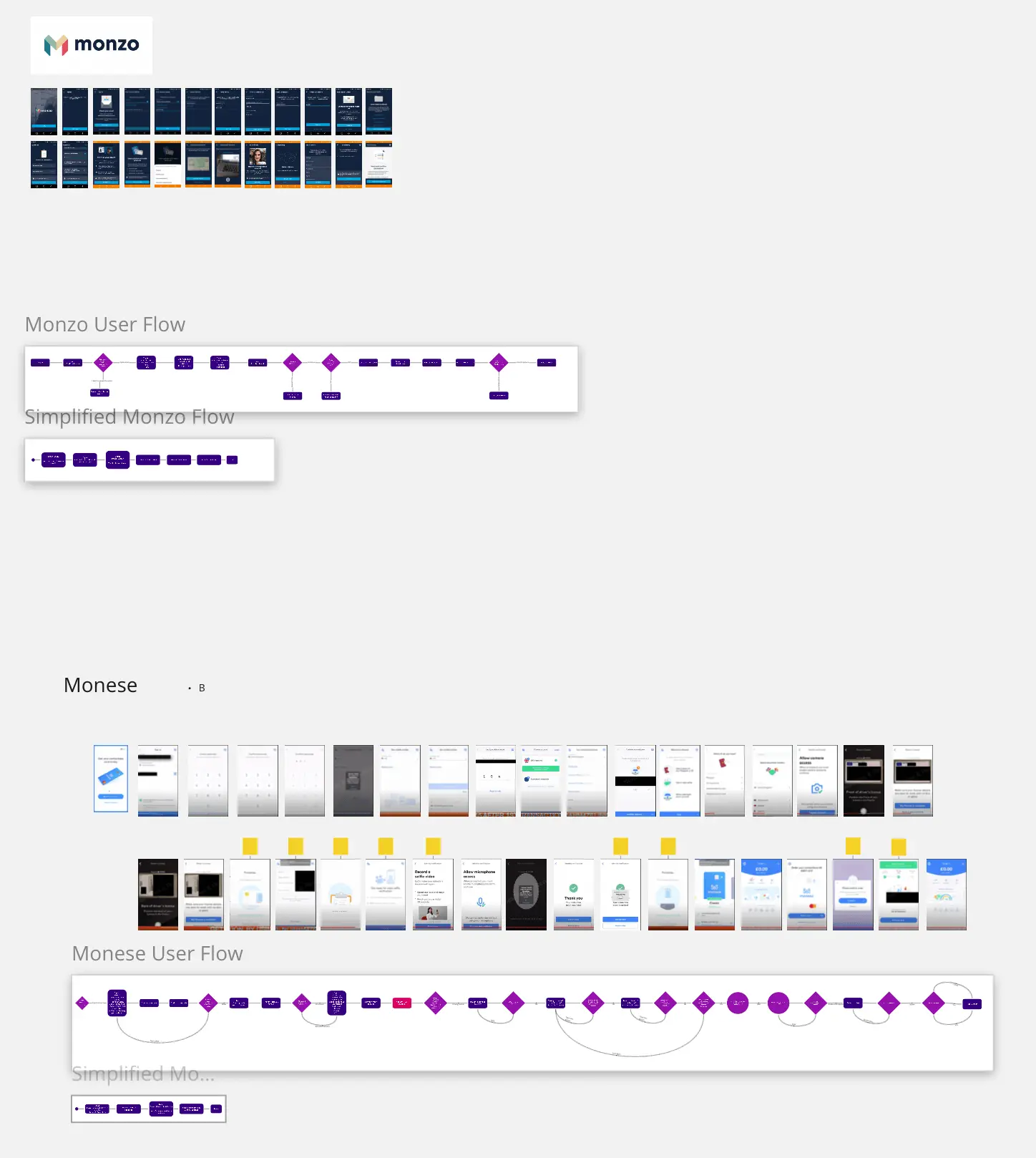

As onboarding was the biggest problem, we decided to tackle that first. After gathering all the screenshots of onboarding of all these neobanking apps, we reverse engineered the user flows and simplified them. This gave us an idea of similiarities between their onboarding strategies.

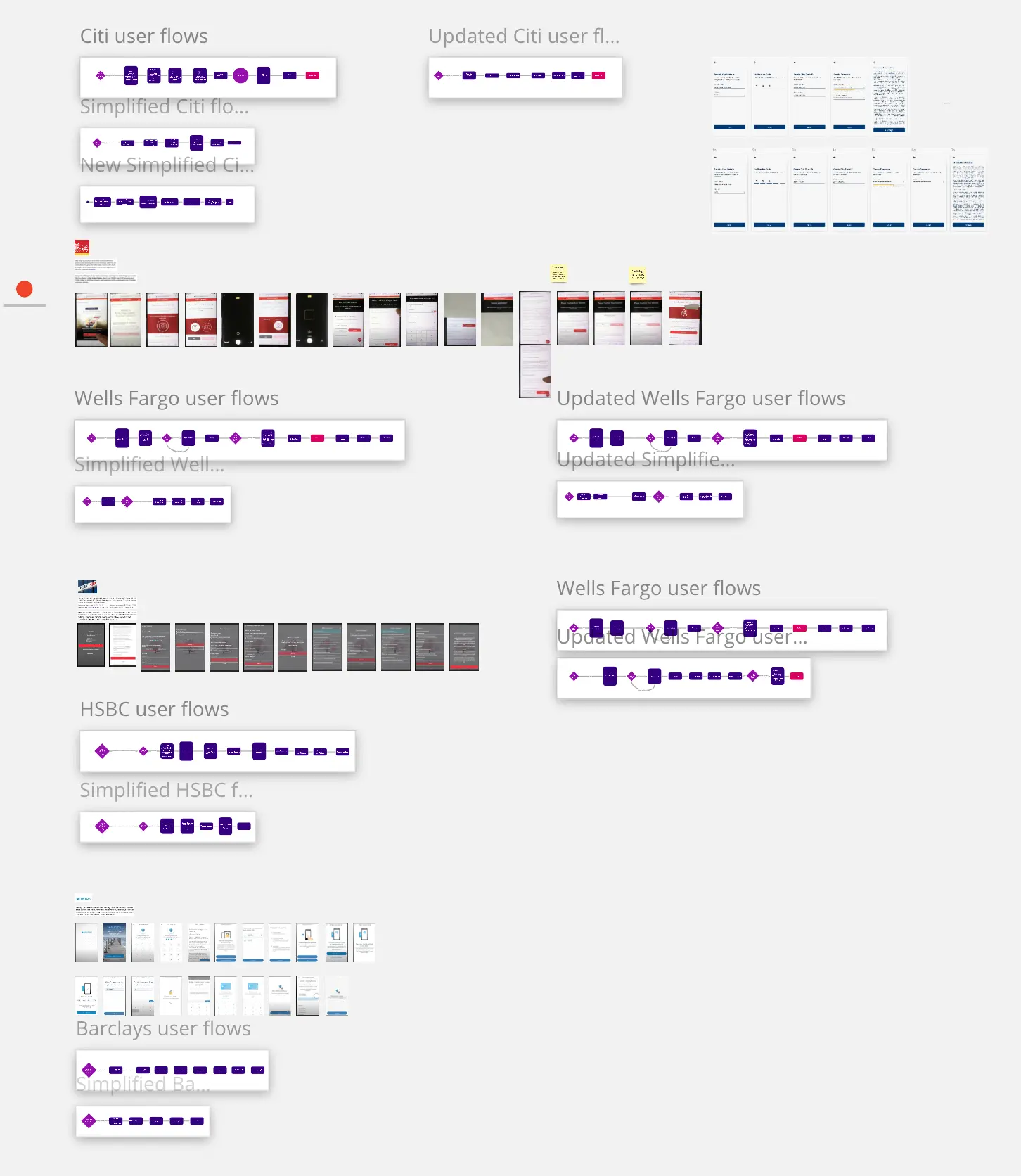

The same exercise was done on traditional banks as well. There wasn’t one to one correlation always e.g in onboarding some traditional bank mandate a prior physical meeting while none of the neobanks had such process. But it was easy to see that traditional banking apps were designed for developers not users. This is a common issue which I have seen at multiple occasions and having been developer myself I sympathize to its causes to an extent.

When a team doesn't have a proper design process and leadership in place, then the question of "what's easier or efficient to build" is often confused with "what's easier to use". It also happens when design is not involved from the start. System flow is different from user flow and while there needs to be a strong cohesion, one is not more important than the other.

We then compared these two flows to extract out an optimized user flow which traditional banks can benefit from.

Then converted the optimized user flow process which we got us to wireframes

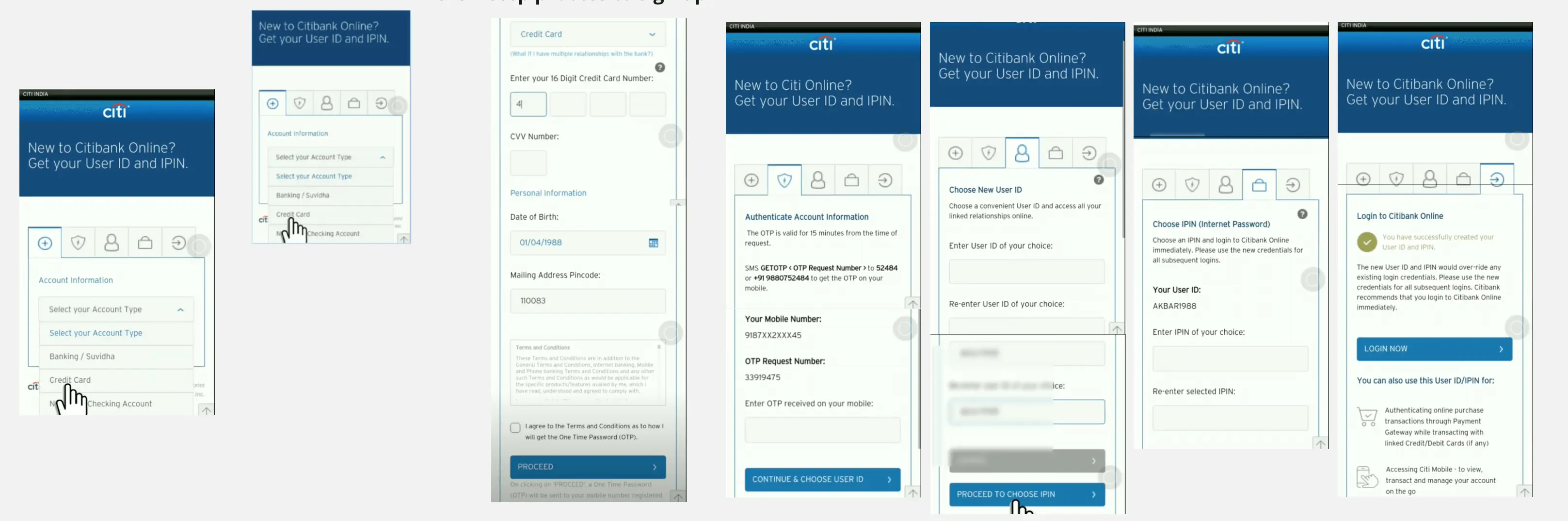

Then the wireframe was applied on a test case. For that we choose citibank’s onboarding process. It looked something like this earlier

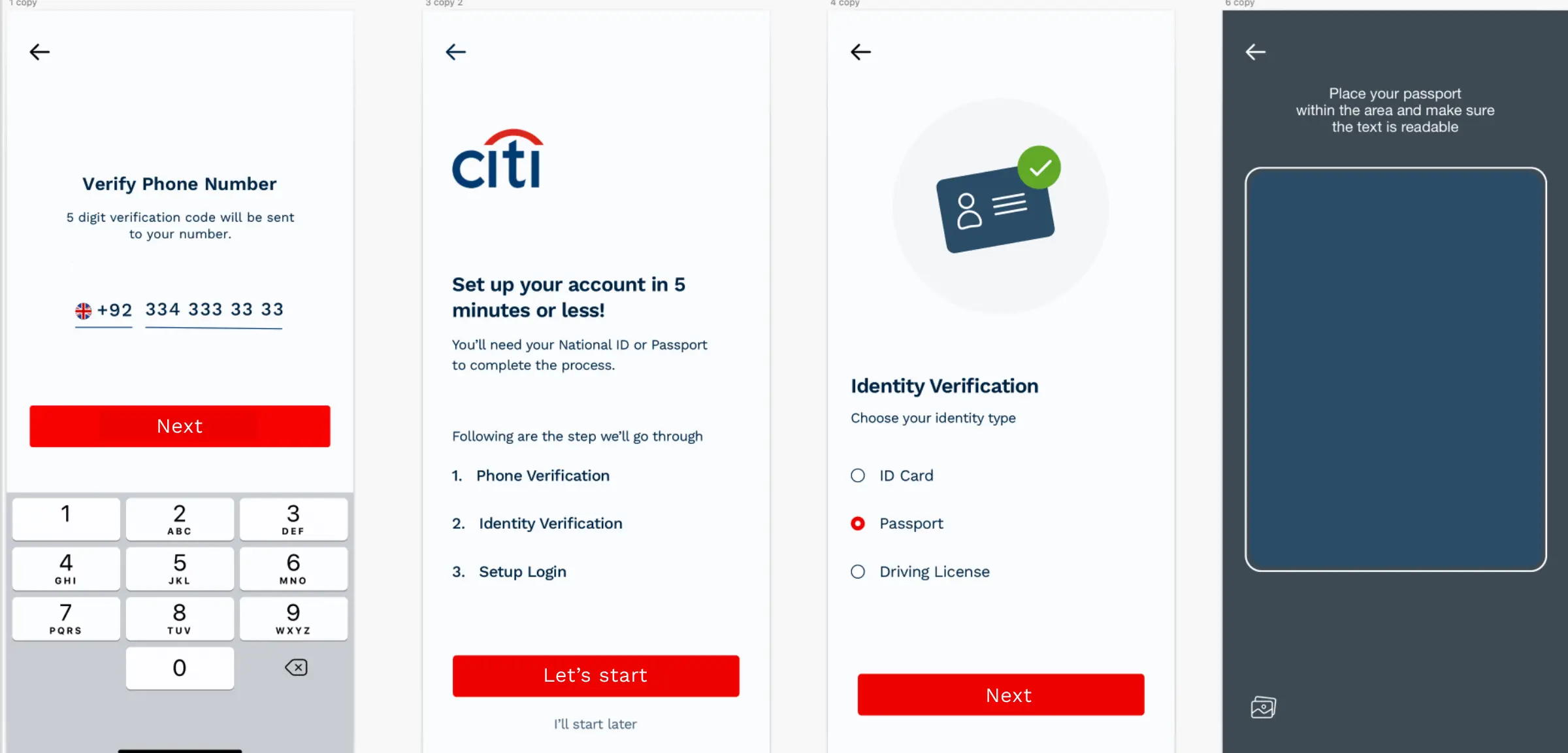

After we applied the learnings from the Neobanks, it looked something like this:

Miro is ❤️

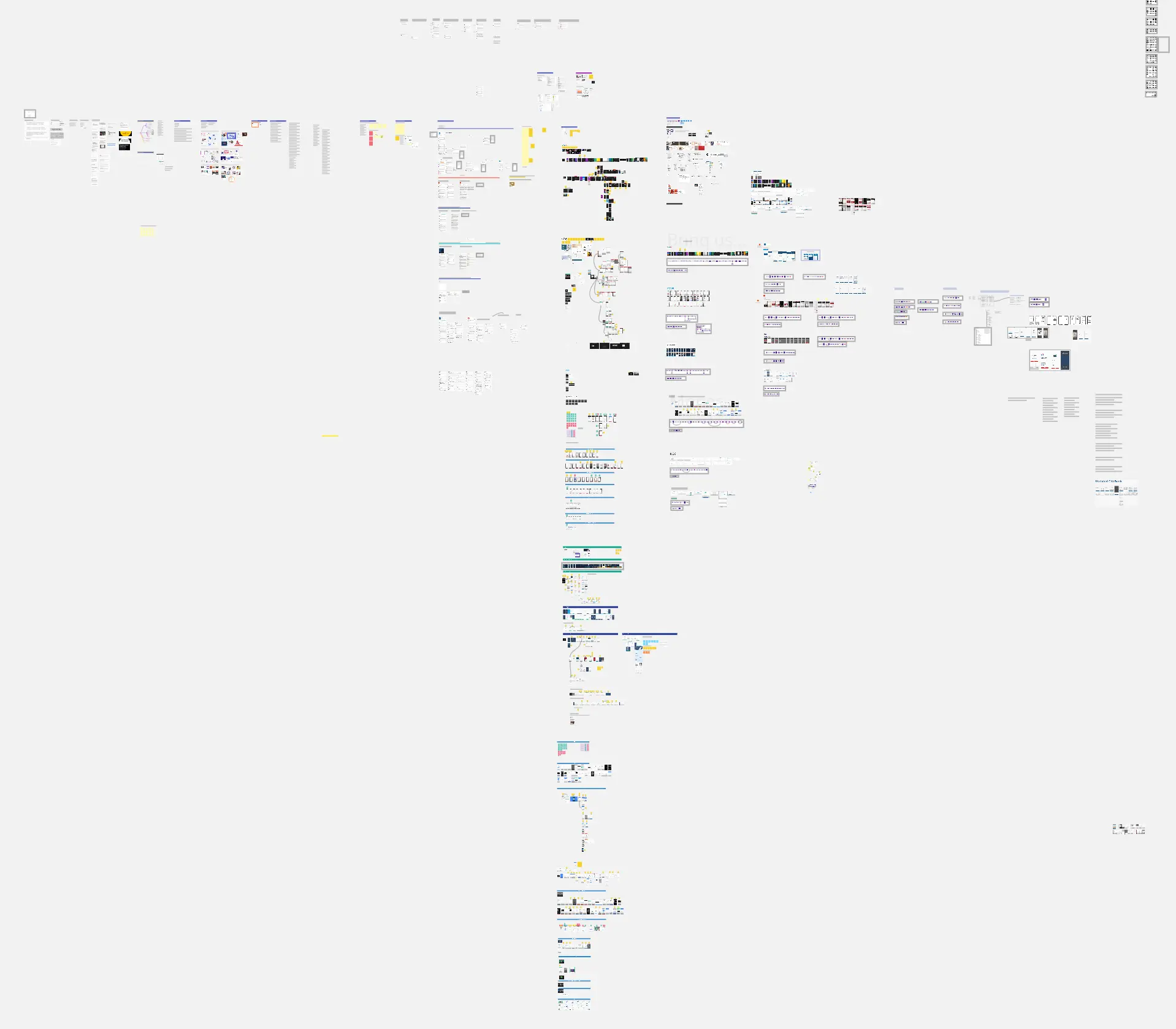

Following is the screenshot for entire miro board. I call it “The Banking Tap”

It also loads up pretty nicely.

A few words